Just Skimming | 3/19

A collage of my weekend newspaper reading and YouTube watching. I hope you find it useful, informative and even slightly entertaining

All about Silicon Valley Bank

If you read or watch nothing else regarding the recent Silicon Valley Bank drama, let it be this new Frontline documentary, The Age of Easy Money, which puts the current banking crisis in contemporary historical context and locates its proximate causes in the Federal Reserve’s policy of lowering interest rates.

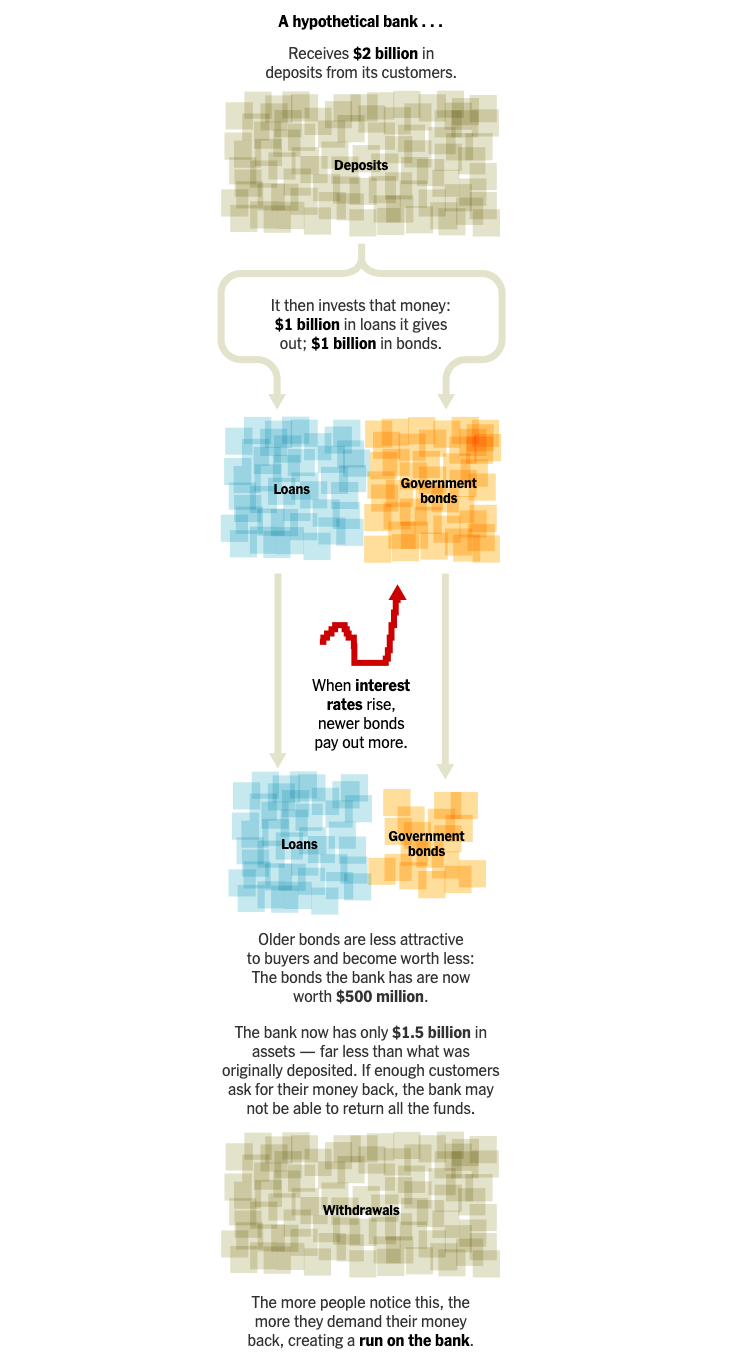

In “Rising Interest Rates And Big Paper Losses Are at Heart of Crisis,” New York Times reporters explain the recent collapse of Silicon Valley Bank:

The bank used its customers’ deposits to buy bonds “back when interest rates were low. Over the past year, the Federal Reserve has raised interest rates eight times to combat the highest inflation in generations. As rates went up, newer versions of bonds became more valuable to investors than those SVB was holding. With the tech industry cooling, some of SVB’s customers began withdrawing their money. To come up with the cash to repay depositors, SVB sold $21 billion of bonds. The bank racked up nearly $2 billion in losses.”

The losses “set off alarms with inventors and some of the bank’s customers,” prompting a classic bank run. There’s also a useful graphic to accompany the story:

In “Can We Slow This All Down, Please?” Ezra Klein, writing in the New York Times, says the fall of Silicon Valley Bank reflects the reality that the Federal Reserve’s low interest rates, which fueled an era of easy money, have come to an end.

SVB’s collapse also took place in a very fast world in which “digital information and digital banking mean bank runs can happen — and spread to other institutions — at astonishing speed. As Gillian Tett noted at The Financial Times, ‘One remarkable detail about the S.V.B. debacle is that, in a few hours last Thursday, about $42 billion (one-quarter of S.V.B.’s deposits) left the institution, mostly through digital means.’”

And thirdly, bank regulators haven’t proven themselves capable of holding financial institutions accountable, leading Klein to this conclusion:

“Banking is a critical form of public infrastructure that we pretend is a private act of risk management. The concept of systemic risk was meant to cordon off the quasi-public banks — the ones we would save — from the truly private banks that can be mostly left alone to manage their liabilities. But the lesson of the past 15 years is that there are no truly private banks, or at least we do not know, in advance, which those are.”

Boring is the new cool?

In “Buying the Dips Can Be Fatal—Unless You’re in It for the Long Term,” Steven M. Sers, head of a specialized asset-manager firm, writes in Barron’s:

“Uncle Sugar, as soldiers have long referred to the U.S. government, has demonstrated once again that he will protect investors from their misplaced avarice [...] At some point, Uncle Sugar will be overcome by events, or OBE. When that happens, the dip buyers will be crushed. It is hard to know when that might happen, but this is a fact. Bond market volatility is now extreme. The odds of a soft or hard economic landing are hard to determine. That should make everyone nervous. What is the countermeasure to chaos and risk? Discipline.”

—

In “SVB shows why we should worry about a ‘cool’ bank,” columnist Anne-Sylvaine Chassany, writing in this weekend’s Financial Times, points out SVB boss Greg Becker’s tendency to describe his job as cool because he gave out easy money to the cool, smart kids of Silicon Valley.

“It is tempting to downplay the risks of providing cheap bridge loans to start-ups before the next round of fundraising or a listing, when everything tech has been so popular. But when interest rates and easy money stopped being available, the flaws in SVB’s model became apparent. Another problem was that the bank overlooked the important but boring job of risk management. [...] Many lessons will be drawn from the demise of SVB, including from the regulatory point of view. What is certain is that it ends the myth of the cool bank. ‘Boring is good if it means safe,’ [economics professor Richard] Holden said.”

—

In “Will the Fed Keep Tightening as Banks Fail?,” columnist Jeff Sommer writes in the New York Times:

“Quantitative tightening is supposed to be boring. That’s by design. It doesn’t demand attention like a bank failure, emergency government rescue, wildly fluctuating interest rates of uncomfortably high inflation. But it is the most important Federal Reserve program you rarely hear about.

“At its core, it involves reducing the more than $8 trillion — yes, trillion — in bonds and mortgage-backed securities held by the Fed, along with draining money from the financial system. All this shrinkage is part of the Fed’s efforts to quell inflation, which is running at 6 percent a year.

“Treasury Secretary Janet L. Yellen once said the slimming process should be as dull as ‘watching paint dry.’ Jerome H. Powell, her successor as Fed chair, said it was so straightforward that it should be on ‘automatic pilot’ and wouldn’t merit close scrutiny. They were both being optimistic, if not entirely disingenuous, I’d say.

“Keeping the enormous asset reduction program boring in a year like this will be a remarkable accomplishment — like parading a barely tamed elephant through city traffic. At any moment, someone could be trampled.”

The weight of history

Screenshot of a photo spread in the Wall Street Journal this weekend.

“What is the weight of history? For Stephanie Wright, it’s as slight as the thinnest of books, a 259-page volume that has upended her life for months and set her on an unusual and determined quest for recognition. She appealed to the Justice Department and some of the highest-ranking officials and judges in the federal court system in the Midwest. None of it had anything to do with what was in the book. It’s what was left out that bothered her – her name.”

From “A Retired Black Prosecutor’s Quest for Recognition,” by Trip Gabriel, the New York Times, on the saga of Stephanie Wright, the first Black assistant United States attorney in the Northern District of Iowa.

—

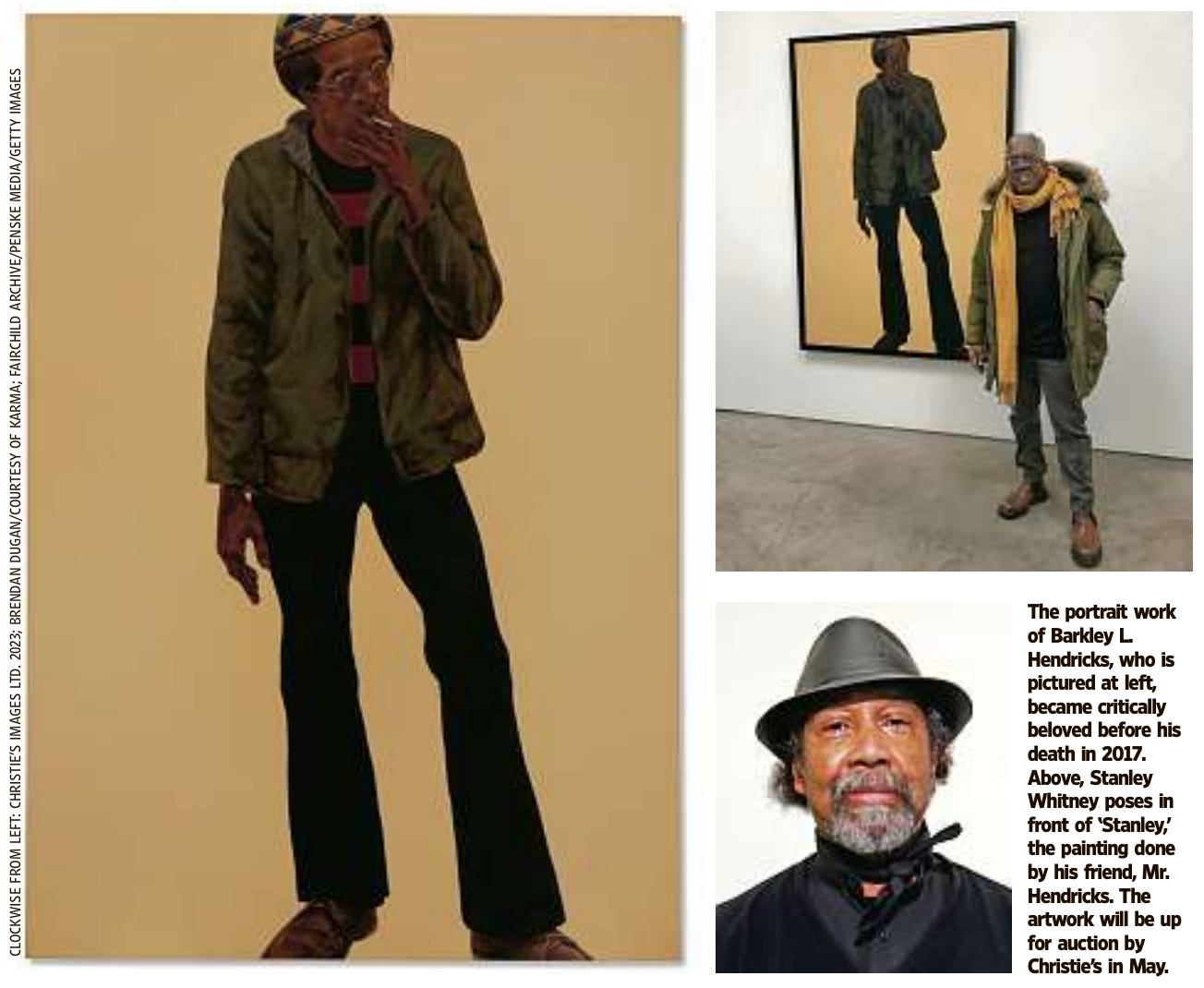

Artist Stanley Whitney, speaking on his friend, the late, great artist Barkley L. Hendricks, in “The Friendship Behind a $5 Million Barkley L. Hendricks Painting,” which appeared in the Wall Street Journal over the weekend.

“He wasn’t out to be revolutionary. He just wanted to paint people he loved,” Mr. Whitney said. “He wanted to see Black people exhibited in those museums.”

Mutu vs. machine

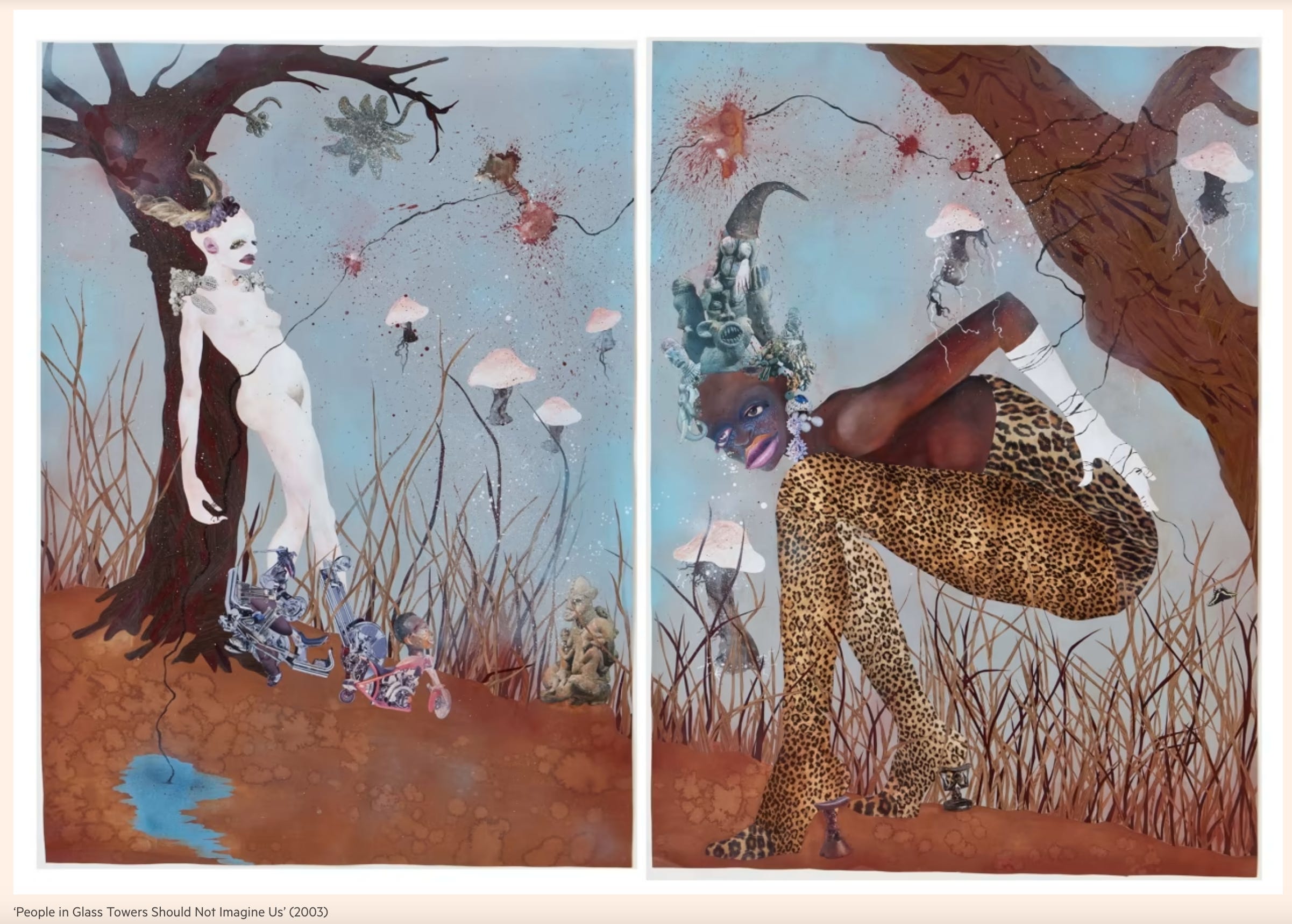

Art by Kenyan artist Wangechi Mutu in the Financial Times this weekend.

These following news briefs and tidbits all appeared in this weekend’s Financial Times, which I read in print (hence no hyperlinks). While divergent, they all share a common thread:

“OpenAI released GPT-4, its latest artificial intelligence model that it claims exhibits ‘human-level performance’ on several academic and professional benchmarks, such as the US bar exam and the SAT school exams.”

—

“Meta [i.e., Facebook] announced plans to axe a further 10,000 jobs as the $469bn social media group’s chief executive Mark Zuckerberg continues to cut costs in what he has called a ‘year of efficiency.’”

—

“PwC [accounting firm PricewaterhouseCoopers] revealed a chatbot experiment with start-up lawyers on tasks such as analysing contracts, in the latest test of [AI] by service firms.”

—

“As Venezuela prepared for carnival season last month, [two news reports featuring newsreaders with American accents provided good news for the country’s controversial president, Nicolas Maduro]. But the two stories were fake, and the two newsreaders do no exist. They are avatars, based on real actors, generated using technology from Synthesia, an artificial intelligence company based in London. Their American accents were synthesised, their talking visages generated by machine-learning algorithms.”

—

“She cut little tiles out of porn stills, nature photos, medical texts, fashion shoots and magazine illustrations, then composed them into bristling hallucinations. Lately, we have been gobsmacked by artificial intelligence’s collagist tendencies, the curious ability of a fake mind to smash together fragments from a vast trove of remembered images into pictures that are at once new and weirdly familiar. The process is analogous to Mutu’s but her creations show just how much catching up robots have to do before they can emulate her powers of recombination and exultant overload.”1

The week in absurdity

Photo by Anton Darius on Unsplash

“As he rose through SVB’s ranks, he relied on a coach to improve his empathy.” (A description of Greg Becker, the former CEO of Silicon Valley Bank, in the weekend Financial Times.

—

Also from the weekend Financial Times: “MindGeek, one of the largest porn companies and the parent of Pornhub, was acquired by Ethical Capital Partners, a newly set-up Canadian private equity firm. No price was disclosed but it comes as MindGeek faces legal action over sexually explicit videos of minors found on its sites.”

—

“We’ve come to a point where many people think it’s natural to have strawberries in winter,” said Satoko Yoshimura, a strawberry farmer in Minoh, Japan, just outside Osaka, who until last season burned kerosene to heart her greenhouse all winter long, when temperatures can dip well below freezing. But as she kept filling up her heater’s tank with fuel, she said she started to think: ‘What are we doing?’

[...]

‘It would be nice,’ she said, ‘if we could just make strawberries when it’s natural to.’”

From “Behind Allure Of Sweet Fruit Is a Bitter Fact” by Hiroko Tabuchi, in this weekend’s New York Times.

Quotable

“Government money flows to private companies in a way that allows the state to put its thumb on the scale but makes people in the industry feel as if they did it all alone.”

Margaret O’Mara, University of Washington history professor and author of The Code: Silicon Valley and the Remaking of America, in an interview for George Hammond’s and Elaine Moore’s “Bailing out small tech” in the weekend Financial Times.

This passage is from Ariella Budick’s profile of Kenyan artist Wangechi Mutu in this weekend’s Financial Times.